RESULTS

Under our institutional cost data and model assumptions with a 1% annual failure rate for MBT implants, an annual failure rate of 1.6% for APT components would be required to achieve equivalency in cost. Over a 20-year period, a failure rate of >27% for the APT component would be necessary to achieve equivalent cost compared with the proposed failure rate of 18% with MBT components.

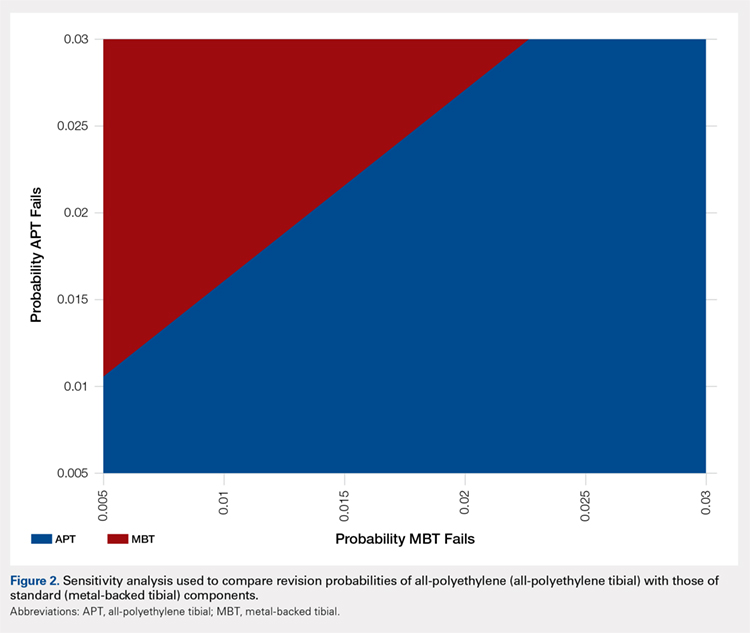

A two-way sensitivity analysis for probabilities of failure was performed to compare revision probabilities of the APT with those of MBT components. The preferred strategy graph is included in Figure 2. This graph shows how varying annual revision rates for both the APT and MBT would impact which option would be preferable. For example, on the graph, an annual failure rate of 1.6% for APT implants would be cost equivalent to a 0.1% annual failure rate for MBT implants at 20 years. A 2.0% annual failure rate for the APT would be equivalent to a 1.4% annual failure rate for the MBT, and a 2.5% failure rate for the APT would be equivalent to a 1.8% MBT failure rate. Holding the APT failure rate constant at 2.5%, any MBT failure rate <1.8% would make the MBT the more cost-effective option, whereas a failure rate >1.8% would make the MBT less cost-effective than the APT. For probability combinations that fall in the lower right area of Figure 2, the APT is preferable, and for probability combinations that fall in the upper left area, the MBT is preferable. The line separating the 2 areas is where 1 would be indifferent, such that the cost per additional QALY is the same for both procedures.

DISCUSSION

In light of the current economic climate and push for cost savings in the United States healthcare system, orthopedic surgeons must increasingly understand the realities of cost and the role it plays in the assessment of new technology. This concept is especially true of TKA as it becomes an increasingly common operative intervention. Utilizing cost savings techniques while ensuring quality outcomes is something that needs to be championed by healthcare providers.

Ideally, the introduction of a new medical technology that is more expensive than preexisting technology should lead to improved outcomes. Multiple randomized radiostereometric and clinical outcome studies looking at failure rates of APT compared with MBT have consistently suggested equivalence or superiority of the APT design when modern round-on-round implant designs are utilized.7-17 Two recent systematic reviews demonstrated that APT components were equivalent to MBT components regarding both revision rates and clinical scores.1,18 Given these results, it seems that the increased use of the APT design could save the healthcare system substantial amounts of money without compromising outcomes. For example, in 2006 Muller and colleagues19. proposed a possible cost savings of approximately 39 million dollars per year across England and Wales, if just 50% of the 70,000 TKAs performed annually used APTs. Our study, which helps quantify the potential cost-effectiveness of the APT design in terms of revision rates, should help further support this debate and provide a framework for the evaluation of new technology.

It should be noted that the results of this current study are based on both assumptions and generalizations. Institutional cost data is known to vary widely among institutions and our conclusions regarding comparable revision rates would change with different cost inputs. We are also unable to take into account individual patients, surgeons, or specific implant factors. It is very difficult to place a price on quality-adjusted life years and negative repercussions with revision surgery. Furthermore, speaking specifically about surgical technique, each surgeon has his/her own preference when performing TKA. There is a lack of intraoperative flexibility when using monoblock tibial components that many surgeons may find undesirable. A surgeon is unable to adjust the thickness of the polyethylene insert after cementation of metal implants. Finally, we are aware that cost-effectiveness analyses cannot take the place of rational clinical decision making when evaluating an individual patient for TKA. Patient age, body mass index, and deformity are all factors that may dictate the use of MBTs in an attempt to improve outcomes.

The results of this analysis help quantify the cost-effectiveness of the APT. Given the additional cost, the MBT design would have to lower revision rates substantially when compared with the APT design to be considered cost-effective. Multiple clinical studies have not shown this to be the case. Further studies are required to help guide clinical decision making and define the role of APT components in TKA.